Hold Fast!

TLDR – don’t panic sell your investments, if you think you have to cash out soon, get advice. This shall pass, you need to Hold Fast.

I am not sure why this came to mind. I was working through the myriad of emails of people (rightly) concerned about their investments, and somehow the idea of a storm at sea came to mind, and then like it does my mind wandered to a movie, and this movie was Master and Commander. In that movie as a storm hits, they all shout at each other to “HOLD FAST”, and what I remember is one old sailor who has it tattooed on his knuckles, as he holds fast to a rope.

I am not quite that old sailor but the lesson passed down to me from those who have come before is essentially this. It’s a storm, it will pass so hold fast. Panicking or trying to change course now will make it worse.

Rationally I think we all know that this will pass. If you lived through SARS, the Global Financial Crisis, Y2K, the dot com bubble, Iraq war (1 and 2), the 87 crash and so on, you know this rationally. But when you are in the middle of the storm, it feels worse.

This feels different, because we forget what it was like before.

And this has happened to me as well. My head and brain know to leave my KiwiSaver but the heart and emotions is wondering if there is a way to fix it, or minimise this.

So lets look at some numbers on my own fund.

I am in the High Growth fund, which is a 98/2 fund split between growth and conservative assets, which is the right plan for me, as I have a house so its just a retirement fund and I a decades from accessing any of the money. This means higher returns when its good and bigger drops when its bad, but overall its better for me.

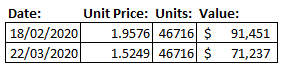

At the market high for this fund on the 18th of feb, I had a balance of $91 000, and today, the 22nd of March its $71 000. So this is a brutal and while I know it will go back up and beyond, its hard. I enjoyed seeing the balance at 90K, and I am dreading seeing it go down below 70K, but it might happen.

On the image below can see that the unit price has dropped from 1.9576 to 1.5249, but my number of units has not gone down.

So that’s my ‘loss’ it’s a paper loss. But right now my fund is on sale. If I put $100 in tomorrow, I will buy 65 units, but a month ago I would have only gotten 51.

What does this mean?

Well when the unit price gets back to where it was a month ago, my additional 14 units get me another $28. So the lower price is helping me long term as I deposit more as you can see in the image below. Now of course as the fund continues to grow further, those extra units will gain me even more. In this basis, volatility (the up and down) is not a big deal.

How much have I actually lost, and how to guarantee a loss:

Currently I have lost no real money, the value of my fund is simply lower. To make the loss real I would move my fund from Growth down to conservative or cash or (if I could) withdraw the fund.

This would involve selling the units at their current lower price, which means there is nothing to grow, when it recovers.

So if you want to make sure you lose money, change your fund down or withdraw your money.

What if its different for you?

This should be true for everyone, unless you need the money very soon. The scenarios I can think of are:

You are about to settle on a house and need to get your KiwiSaver out

You are about to retire and need to get all of your money out to pay off debt etc

You have lost your job (or are about to) and don’t have any savings to cover you so need to do a hardship withdrawal.

In these cases you need to assess how much you really need to get the money out, and you need to be very aware of the fact that any loss you think you have now is locked in, you wont be able to have the fund recover.

Make sure you get personalised advice in this case.

Summary:

I know this feels different, I know this feels scary, but you need to Hold Fast. This too shall pass.

I hope this analysis of my personal numbers helps a little to clarify how this all works

If you need more advice, please get in touch.